Before EOI

Confirm refundability, priority logic, launch timeline, current RERA status, and whether payment is into an official disclosed account.

Move from brochure rates to livable commitments, then verify RERA and payment safety before any EOI.

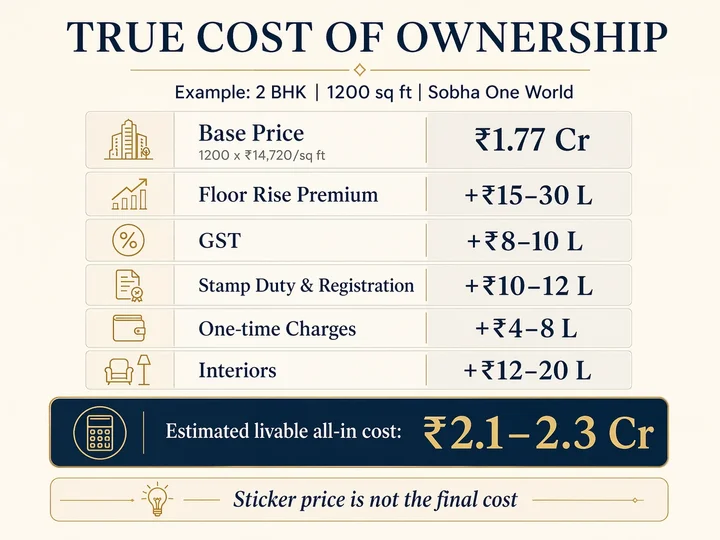

The most useful way to read Sobha One World pricing is to separate three numbers: the brochure number, the transaction number, and the livable number. The brochure number is the base apartment price that appears in launch conversations, such as a pre-launch base rate around ₹14,720 per sq. ft. and an indicative range from about ₹1.09 Cr to ₹3.9 Cr. The transaction number adds floor rise, preferred location charges, parking, clubhouse, corpus, legal, infrastructure, GST, stamp duty, registration, and other statutory or project charges. The livable number adds interiors, appliances, moving costs, and the buffer needed to operate the home after possession.

This distinction matters because the project sits in a high-ticket band. A 1,200 sq. ft. 2 BHK at ₹14,720 per sq. ft. gives a base price near ₹1.77 Cr before extras. Once a buyer adds tax, government charges, project charges, and a modest interior budget, the realistic outlay can move toward the ₹2.1-2.3 Cr band. That does not make the project unaffordable by itself; it simply means the affordability test must be done on the final landed cost, not on the lowest figure shown in a lead advertisement.

The same logic applies to larger homes. A 3 BHK Lux or Grande may look reasonable on a price-per-square-foot comparison with Whitefield or Panathur, but the total cheque size changes the buyer’s risk profile. A family buying a 3 BHK at more than ₹2.5 Cr must plan for down payment, rent during construction, pre-EMI, school fees, insurance, emergency corpus, and interiors without depending on quick rental income after handover. A 4 BHK buyer has even more reason to check liquidity because premium resale pools are smaller and more sensitive to market cycles.

As of 25 April 2026, treat every public price as indicative until it is matched against a dated official price sheet. Ask whether the quoted price is base price only, whether GST is included, whether car parking is mandatory and separately charged, whether floor rise starts from a particular level, whether clubhouse and maintenance corpus are fixed or variable, and whether launch-period discounts are written into the allotment letter. Spoken discounts are not enough for a five-year commitment.

A balanced pricing view is this: Sobha One World may still be cheaper per square foot than mature Sobha or comparable premium options in stronger Whitefield-side locations, but it is not a low-budget project. The buyer is paying for brand, township scale, future Hoskote upside, and a long delivery runway. The value question is not “is it cheap?” but “is the risk-adjusted all-in price better than what the same buyer can buy today in Budigere, Whitefield, KR Puram, Sarjapur Road, or North Bangalore?”

| Configuration | Current public size band | Indicative planning range | Budget note |

|---|---|---|---|

| 1 BHK | 740 sq. ft. | ₹1.09-1.15 Cr | Lowest entry ticket, but resale audience is more investor/single-professional driven. |

| 2 BHK Small | 1,070 sq. ft. | ₹1.5-1.7 Cr | Better ticket control, but check bedroom size, utility, storage, and future family fit. |

| 2 BHK Large | 1,200 sq. ft. | ₹1.73-1.9 Cr | Likely the broadest end-user/rental audience if cost remains comfortable. |

| 3 BHK Lux | 1,525 sq. ft. | ₹2.25-2.28 Cr | Family-oriented size; confirm study/utility/maid-room interpretation in plan. |

| 3 BHK Grande | 1,825 sq. ft. | ₹2.7-2.9 Cr | Stronger liveability, higher EMI, and a narrower but premium resale pool. |

| 4 BHK Lux | 2,100 sq. ft. | ₹3.1-3.4 Cr | Lifestyle purchase; budget interiors and holding cost carefully. |

| 4 BHK Grande | 2,500 sq. ft. | ₹3.6-3.9 Cr | Premium family product where tower, view, and floor selection matter heavily. |

The price sheet should be read configuration by configuration, not as one blended range. The 1 BHK is not competing with the 4 BHK Grande. It is competing with smaller branded apartments, rental-investment products, and possibly a lower-ticket resale option in a more mature location. The 2 BHKs compete with family starter homes in Whitefield-adjacent corridors. The 3 and 4 BHKs compete with larger end-user homes, premium Budigere launches, and selected resale units in established East Bangalore communities.

The small 2 BHK is often attractive because it limits ticket size, but buyers should confirm whether the layout feels compact after furniture, work-from-home requirements, and storage. A floor plan can look efficient in a brochure while still feeling tight when two adults work from home and a child needs a study zone. The large 2 BHK typically has the best balance for many families because the extra 130 sq. ft. can support more comfortable bedrooms, better circulation, or a more usable living-dining space.

The 3 BHK Lux and 3 BHK Grande require a different lens. These homes are less about “can I enter the township?” and more about “will this be enough home for ten years?” Buyers should check whether the third bedroom is genuinely usable, whether the kitchen and utility support full-time family use, whether balconies are meaningful or ornamental, and whether the maid/study label in marketing corresponds to the actual usable space in the plan.

The 4 BHK plans should be evaluated like long-term lifestyle homes. The premium is not only in area; it is in view, privacy, arrival experience, storage, lift access, parking, and ability to host family. At this ticket size, a small difference in floor, orientation, or tower position can materially affect resale and living satisfaction. The correct comparison may not be another Hoskote apartment; it may be a villa, a resale Sobha/Prestige unit in a stronger location, or a larger apartment in Budigere Cross.

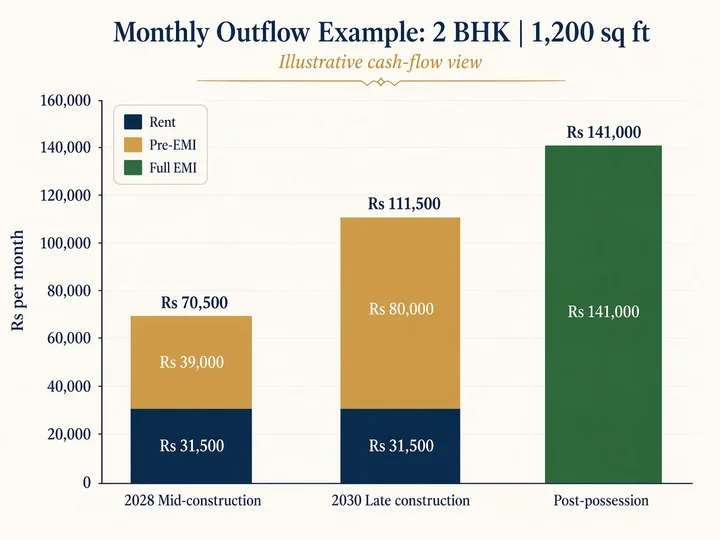

The most common affordability mistake is to calculate only the final EMI and ignore the path to possession. Sobha One World is expected to follow a construction-linked payment logic where the buyer pays a booking amount, a larger amount around the Agreement of Sale stage, and the remaining amount through milestone-linked slabs. This is better than paying most of the amount upfront, but it still creates a rising pre-EMI burden as the bank disburses more money.

Use a simple example. If a 2 BHK has an all-in cost near ₹2.1 Cr and the buyer funds 80 percent through a home loan, the loan amount is around ₹1.68 Cr. At an 8 percent interest rate over 20 years, the full EMI is roughly in the ₹1.4 lakh per month zone once the loan is fully disbursed. If the buyer is currently renting, the construction period can involve rent plus pre-EMI, not rent instead of EMI.

At mid-construction, if the bank has disbursed ₹70 lakh, the interest-only pre-EMI at 8 percent is roughly ₹46,000 per month before considering any principal repayment plan. If the disbursal rises to ₹1.2 Cr closer to 2030, the interest component can move near ₹80,000 per month. Add a current rent of ₹30,000-45,000 in Whitefield, KR Puram, Kadugodi, Bellandur, or a similar work-linked area, and the household outflow can become uncomfortable even before possession.

This does not mean the buyer should avoid the project. It means the buyer should choose a configuration that remains safe under stress. Run three scenarios: salary grows as expected, salary is flat for two years, and one income is interrupted for six months. If the home is still manageable in the second and third scenario, the purchase is financially healthier. If the plan only works with promotions, rent increases, or resale appreciation, the buyer is using hope as a financing tool.

A second cash-flow issue is interiors. Many buyers postpone interior budgeting because possession feels far away. That is understandable, but the eventual amount is real. A modest 2 BHK interior can still run into lakhs for wardrobes, modular kitchen, lighting, appliances, safety grills, curtains, false ceiling choices, and furniture. Larger 3 and 4 BHK homes can turn interiors into a separate loan-sized event. Build this into the livable cost today so possession does not become another financial shock.

Confirm refundability, priority logic, launch timeline, current RERA status, and whether payment is into an official disclosed account.

Match unit, tower, carpet area, phase name, payment milestones, delay clauses, and completion date against the RERA listing.

Ask the bank what it will fund, when disbursals occur, and whether project approval is final for the exact phase and tower.

EOI is not the same as ownership. It is an expression of interest that may help with priority selection, pricing slab, or allotment sequence, but it does not replace RERA registration, allotment letter, Agreement of Sale, or a complete cost sheet. The public notes mention EOI amounts of ₹5 lakhs for 2 BHK, ₹8 lakhs for 3 BHK, and ₹10 lakhs for 4 BHK. The key buyer question is not only the amount; it is the refund process, deduction clauses, timeline, and whether the amount is adjusted cleanly into the booking schedule.

GST should be treated as a planning item for under-construction property. The common working rate for non-affordable under-construction residential apartments is 5 percent without input tax credit, but buyers should verify current tax treatment with the developer and a tax professional because agreement structure and policy changes can affect interpretation. Registration and stamp duty should also be budgeted separately. Karnataka charges can materially change acquisition cost, and buyers should verify final rates through official or legal channels before registration.

RERA is the central legal checkpoint. Once the project is registered, the buyer should compare the sales conversation with the RERA record: project name, phase, promoter, land area, tower count, inventory, carpet area, common area, sanctioned plan uploads, project bank account, and declared completion date. If a sales executive uses a broader township name while the RERA record uses a phase name such as Sobha One Residences, the buyer should understand exactly which entity and phase are in the agreement.

A price that looks good before RERA can look different after full documentation. Sanctioned plans may define carpet area differently from brochure super built-up area. Payment schedule may have milestones that accelerate cash outflow. Floor-rise, view, and preferred-location premiums may be applied after tower selection. The safest way to avoid surprise is to ask for a complete proforma cost sheet for the exact unit stack before emotionally committing to a configuration.

A pricing page becomes useful only when it helps the buyer say no to the wrong unit. The most dangerous version of affordability is “the bank will approve it.” Bank eligibility is based on income, credit profile, property value, and policy. Household comfort is based on school fees, parent support, job volatility, rent, medical needs, childcare, travel, lifestyle, and emergency savings. Sobha One World buyers should run a comfort test, not only an eligibility test.

Start with the down payment. A ₹2.1 Cr all-in 2 BHK with 80 percent funding still needs about ₹42 lakh in margin money, plus registration timing, interiors later, and liquidity buffer. A larger 3 BHK may require ₹55-70 lakh or more in upfront and staged equity depending on final cost. If the buyer empties emergency savings to make the booking, the purchase is fragile even if the long-term EMI looks manageable.

Next, test rent plus pre-EMI. Many buyers in this project will continue living near work or school until possession. That means the construction period is not free. If rent is ₹35,000 and pre-EMI rises from ₹25,000 to ₹80,000 over time, the household may experience a long period where monthly outflow feels like a second home. This is especially important for dual-income families planning children, elder care, or job changes before 2031.

Then test interest-rate sensitivity. A small change in rate can materially change EMI on a large loan. Buyers should not build the plan on the lowest promotional rate. Use a conservative rate and ask the banker whether the loan is repo-linked, how resets work, what processing fees apply, whether insurance is optional, and whether prepayment penalties are nil for floating-rate loans. The loan terms should be read as carefully as the project brochure.

Finally, test exit. If the buyer needs to sell before possession, who is the likely buyer? What transfer charges apply? Will the developer still have unsold inventory at comparable prices? Will a resale buyer prefer a lower floor, a different tower, or a more mature project? A launch buyer should not assume that a large supply base creates instant resale profit. Liquidity improves when the project shows visible progress and the location story strengthens.

The safe pricing conclusion is not to avoid higher-ticket homes. It is to match ticket size to resilience. If a 3 BHK is comfortable under stress, it may be a better long-term home than a tight 2 BHK. If the 3 BHK requires optimistic assumptions, a 2 BHK Large may be the financially healthier decision. The best unit is the one that leaves the buyer enough cash and calm to enjoy the home when it is finally delivered.

| Stress test | Question | Healthy answer |

|---|---|---|

| Emergency buffer | Can you hold 9-12 months of expenses after booking? | Yes, without depending on resale or family borrowing. |

| Rent overlap | Can you carry rent plus rising pre-EMI for several years? | Yes, under conservative income assumptions. |

| Interior budget | Is possession interior spend already planned? | Yes, as a separate future cash requirement. |

| Rate risk | Does EMI remain safe if rates move up? | Yes, with room in monthly surplus. |

| Exit risk | Can you hold beyond possession if resale is slow? | Yes, the plan does not require a quick flip. |

The first pricing document is the full cost sheet for the exact unit. It should show configuration, tower, floor, unit number, super built-up area, carpet area where available, base rate, base value, floor rise, PLC or view premium, parking, clubhouse, corpus, infrastructure charges, legal charges, maintenance deposits, utility deposits, GST, stamp duty estimate, registration estimate, and total payable amount. If any line item is missing or merged, ask for a clearer version.

The second document is the payment schedule. A construction-linked plan can still be aggressive if milestones come quickly or if early slabs are front-loaded. Ask when each payment is due, what construction event triggers it, how much must be paid before Agreement of Sale, and how bank disbursal will be coordinated. A buyer paying rent should map every milestone to expected monthly outflow.

The third document is the EOI and booking terms. It should state refundability, deductions, timeline, adjustment against booking, what happens if RERA is delayed, what happens if preferred unit is unavailable, and whether the buyer can change configuration. If the EOI terms are informal, the financial risk is higher. A launch-stage expression of interest should be written tightly precisely because the project is still moving from marketing to documentation.

The fourth document is the draft Agreement of Sale once available. Price escalation clauses, delay compensation, cancellation clauses, force majeure wording, carpet area variation, possession definition, maintenance handover, and tax treatment should be reviewed by a lawyer. Buyers often read only the price schedule and miss clauses that affect exit, refund, or possession expectations.

The fifth document is the bank approval or project approval note. A bank’s willingness to fund the project helps, but the buyer should still ask whether approval applies to the exact phase and tower. Also confirm margin requirement, disbursal process, pre-EMI versus full EMI option, mandatory insurance claims, processing fees, and whether the quoted interest rate is final or subject to sanction conditions.

The sixth document is the buyer’s own affordability sheet. It should include down payment, registration timing, interiors, emergency fund, rent, pre-EMI, full EMI, maintenance, property tax after possession, and conservative income assumptions. This personal document is just as important as developer paperwork because it shows whether the project is not only buyable, but sustainable.

A practical way to use this pricing page is to turn it into a meeting agenda. Instead of asking the sales team broad questions such as whether the project is good, ask for the exact all-in cost, EOI, taxes, loan, and payment milestones details that affect your decision. Specific questions get specific answers, and specific answers are easier to compare with documents later.

Keep a written version history. Launch-stage projects change quickly: pricing slabs move, tower availability changes, RERA documents appear, payment schedules are refined, and amenity phasing becomes clearer. When you receive an answer, record the date, person, document name, and whether the answer came from a brochure, email, cost sheet, RERA upload, or verbal discussion.

Do not treat the first available unit as the only opportunity. Large projects often create urgency through EOI windows and preferred-unit availability, but the buyer still needs to check whether that unit fits budget, routine, floor preference, view, and resale logic. A less glamorous unit that fits the decision framework can be better than a rushed premium unit.

The key document for this page is the exact unit cost sheet and construction-linked payment schedule. If that document is not yet available or does not answer the question clearly, mark the item as pending rather than resolved. Pending items do not always mean “do not buy.” They mean the buyer should avoid converting interest into a binding commitment until the uncertainty is proportionate to the amount being paid.

Every Sobha One World decision also has an opportunity cost. The same budget may buy a smaller but more mature Whitefield resale, a different branded Hoskote launch, a Budigere Cross apartment, a North Bangalore option, or a lower-risk ready home. The pricing decision is stronger when the buyer can explain why Sobha One World remains preferable after those alternatives are honestly considered.

The final pricing takeaway is that attractive base pricing can become a much larger livable commitment after statutory charges, interiors, and rent overlap. If that trade-off is acceptable, the next step is to run a household stress test before selecting the final configuration. If it is not acceptable, the buyer should pause, collect more evidence, or compare a different configuration or location before paying further.

The notes below are the compact public source trail used for this page. Project figures remain provisional until matched against the latest developer documents, Karnataka RERA listing, sanctioned plans, and signed price sheet.